When a business needs immediate cash flow, it’s common to consider quick financing options. This is where the key question arises: what is an MCA loan and is it really worthwhile?

When a business needs immediate cash flow, it’s common to consider quick financing options. This is where the key question arises: what is an MCA loan and is it really worthwhile?

Although they are often called “loans”, MCA cash advances are not technically a traditional loan. Instead, they are advanced payments based on the future sales of the business, which implies very different conditions than those of a bank loan.

Key Takeaways

- MCA cash advances are based on future revenue. This means that the real cost is linked to business performance and not to a traditional interest structure.

- Ease of access to this type of financing usually comes with conditions, which can compromise operational stability if not carefully evaluated.

- There are financial relief alternatives that can help reorganize debt, but acting in time is crucial to avoid more serious consequences.

What is a merchant cash advance (MCA)?

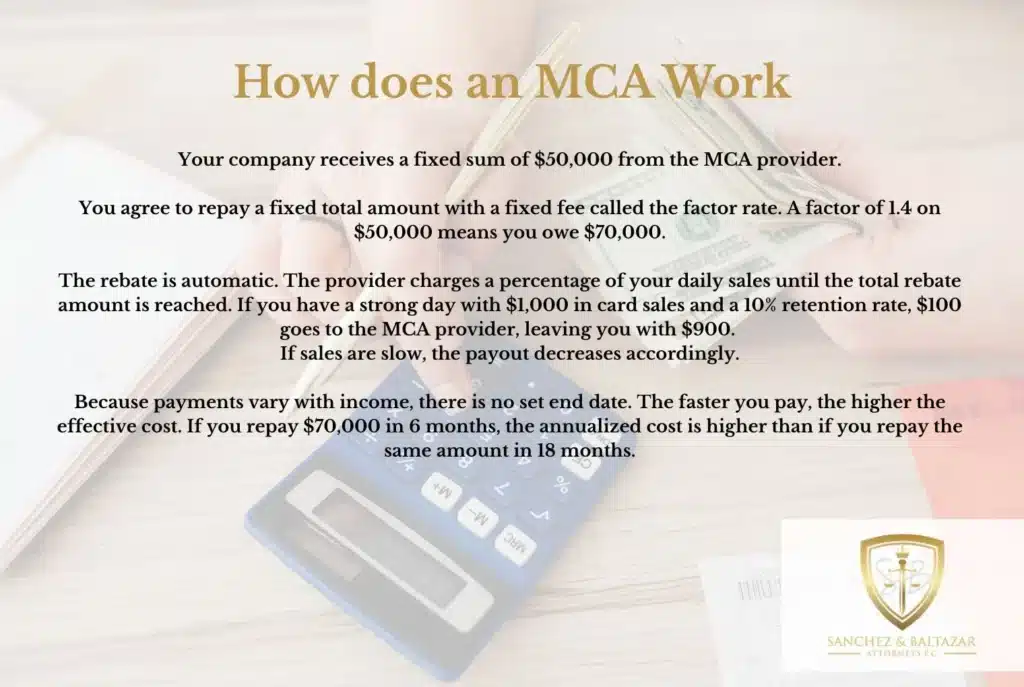

So, what is a merchant cash advance (MCA)? It is an agreement in which a company receives a sum of money upfront in exchange for a percentage of its future revenue. These funds typically come from credit or debit card sales. Instead of paying fixed monthly fees, the business returns the money through automatic daily or weekly deductions.

This type of financing is usually attractive to companies that:

- Do not qualify for traditional bank loans

- Urgently need money

- Have a steady income from card sales.

What are MCA payments?

One of the most important features to understand is: What are MCA payments? Unlike a conventional loan with clear interest rates, the MCAs use a “factor rate” (for example, 1.2 or 1.4). This means that if you receive $10,000, you could end up paying $12,000 or $14,000, regardless of how long it takes to pay it off.

One of the most important features to understand is: What are MCA payments? Unlike a conventional loan with clear interest rates, the MCAs use a “factor rate” (for example, 1.2 or 1.4). This means that if you receive $10,000, you could end up paying $12,000 or $14,000, regardless of how long it takes to pay it off.

These types of loans were originally designed for retailers who typically receive constant sales through credit cards, but today they serve various sectors.

Payments are made via:

- Automatic daily or weekly debits from the bank account

- Retention of a percentage of daily sales

This may seem flexible, but in practice it can put a lot of pressure on the business’s cash flow.

When might it make sense to use an MCA?

An MCA cash advance might be considered in very specific situations, such as:

- Immediate financial emergencies

- Short-term business opportunities with a quick return

- Total lack of access to other forms of financing

However, it should be viewed as a last resort, not a long-term financial strategy. For those interested in this type of financing, there is also the option of using an external provider; however, it’s crucial to ensure the provider is trustworthy and that their terms are clear and straightforward.

They will most likely ask for the company name and type of legal entity; how long it has been in operation; its monthly or annual revenue; the business sector; and recent sales data.

Generally, MCA providers request three to six months of bank statements and debit and credit card processing data. Their goal is to assess how much revenue your company generates.

Do MCAs have any advantages?

The most obvious benefit is the quick access to funds, which can be obtained within 24 hours since the application does not involve an extensive risk assessment nor does it require much documentation.

Furthermore, for businesses that cannot obtain traditional loans or a solid line of credit, MCAs are proving to be an attractive option. Many even consider payment based on future sales to be more convenient and flexible.

Finally, there are not many restrictions regarding the use of the funds and generally no guarantees through physical assets are required.

Disadvantages of MCA cash advances

Although they may seem convenient, MCA cash advances have significant disadvantages:

Although they may seem convenient, MCA cash advances have significant disadvantages:

- High costs: The total cost is usually much higher than that of a traditional loan. The lack of a clear APR rate can make it difficult to understand how much you are actually paying.

- Aggressive payments: Daily or weekly debits can seriously affect cash flow, especially in businesses with variable income.

- Debt cycle: Many businesses end up applying for multiple MCAs to cover the payments of previous ones, entering a spiral that is difficult to break.

- Lack of regulation: Unlike traditional loans, MCAs are not regulated in the same way, which can leave the merchant in a vulnerable position.

What to do if you are already in debt with MCA?

If you are already dealing with the burden of one or more MCAs, there are alternatives to regaining financial control:

In some cases, it is possible to negotiate with the supplier to reduce the total amount owed or establish new payment terms.

It is also possible to renegotiate the debt. This involves modifying current conditions to make payments more manageable, such as extending the term or reducing the frequency of debits.

Combining several obligations into a single monthly payment can simplify management through consolidation, although it does not always reduce the total cost nor is it an optimal solution. It is also possible to obtain specialized legal advice, as some MCA contracts include aggressive or confusing clauses. An attorney experienced in this type of financing can identify abuses and help defend your rights, and that is why we at SB Legal are at your service with a free initial consultation by calling (760) 302-4652.

In any case, whatever you do, reviewing the business model, adjusting expenses, and improving cash flow management is key to avoiding falling back into this type of financing.

Final thoughts

Understanding what an MCA loan is is crucial before agreeing to this type of arrangement. While MCA cash advances can offer a quick fix, their costs and terms can jeopardize a business’s financial stability. Carefully weighing the pros and cons, and knowing what relief options are available, can make the difference between a temporary solution and a long-term problem.

Frequently Asked Questions

Does an MCA affect business or personal credit?

It depends on the provider. Some don’t report to credit bureaus, but if the agreement goes into default or becomes a legal matter, it could impact both the business and personal credit of the owner.

Can an MCA contract be cancelled after it has been signed?

There is generally no standard cancellation period as with other financial products. However, in certain cases, there may be legal or contractual grounds for challenging the agreement.

Do MCAs require a warranty or collateral?

Although they do not always require physical collateral, many include a personal guarantee or clauses that allow the provider to access business assets in case of default.